Earn 9%–15% on Senior Secured Bonds.

Lower risk. Fixed returns. Start investing on Aspero with just ₹10,000.

Explore Bonds

Bonds in India: Risk-and-Return Guide

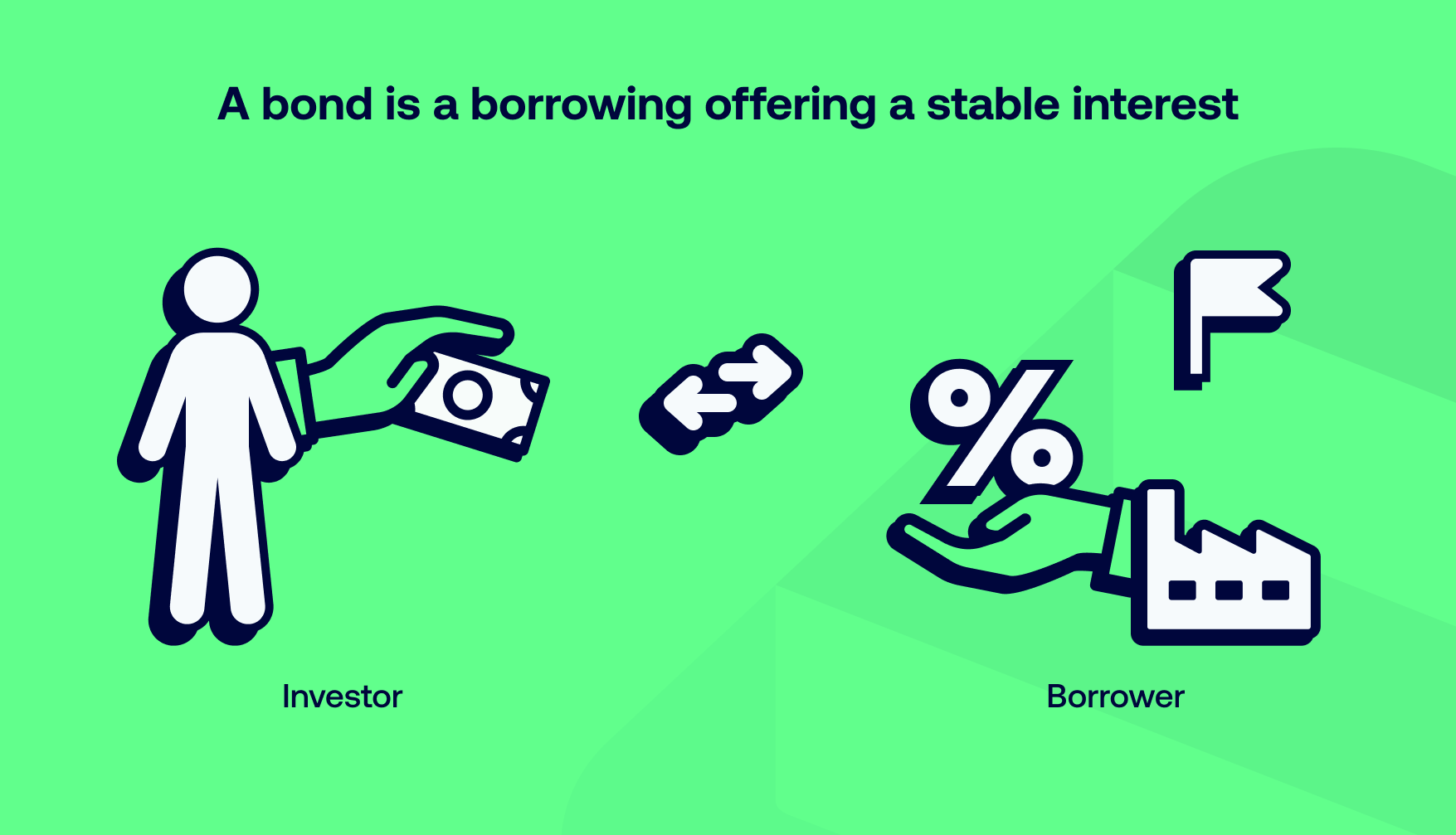

Bonds in India are one of the most underrated fixed-income assets available to Indian investors. They sit between the relatively lower returns of traditional bank fixed deposits and the high volatility of equities — giving you the opportunity to balance safety, income, and growth in your portfolio.

Bonds in India, both government bonds and corporate bonds play an important role in wealth creation. With the rise of SEBI-regulated Online Bond Platform Providers (OBPPs) like Aspero, retail investors can now access bonds digitally with minimum investments starting from just ₹1,000.

With the right understanding of credit ratings, issuer fundamentals, maturity profile, and payout structure, bonds in India can become a reliable and strategic part of your investments.

Credit Rating

Understanding Ratings & Risks of Bonds in India

Credit Rating

Credit ratings (AAA, AA, A, BBB, etc.) indicate the financial strength and repayment capacity of the bond issuer. These ratings are assigned by agencies such as CRISIL, ICRA, CARE Ratings, and India Ratings.

AAA to AA-rated bonds

→ Usually issued by government-backed entities or large NBFCs

→ Lower risk, lower return (typically ~7%–9.5%)

→ Ideal for conservative or first-time investors

Examples in India:

PSU issuers like Power Finance Corporation (PFC), REC Limited, and Indian Railway Finance Corporation (IRFC) often issue highly rated bonds.

A to BBB-rated bonds

→ Often issued by growing companies or NBFCs

→ Higher yields (typically 10%–15%+)

→ Slightly higher risk

→ Suitable for moderate to aggressive investors

Examples: Certain mid-sized NBFCs, infrastructure companies, or real estate-backed issuers.

Pro Tip:

A BBB-rated bond from a company with strong cash flows, no history of defaults, and a short remaining maturity (1–2 years) can offer attractive yields with manageable risk.

Beyond Ratings — What Else to Check

Yield To Maturity

Coupon Rate v/s Yield To Maturity

1. Coupon vs Yield to Maturity (YTM)

Coupon Rate: The fixed annual interest paid on face value.

YTM: The actual annualized return if held till maturity, factoring in current market price and payouts.

➡ Always check YTM, especially when buying bonds in India from the secondary market.

2. Security of the Bond

Bond Security Types

Bond Security Types

Secured Bonds:

Backed by assets like property, receivables, or cash flows. Safer than unsecured bonds.

Senior Secured Bonds:

Have first priority claim on assets in case of default.

Unsecured Bonds:

No specific collateral. Higher risk, therefore higher potential yield.

3. Issuer Due Diligence

Company Results

Before investing, review:

-

Default history (if any)

-

Revenue & Profit After Tax (PAT) trends

-

Asset Under Management (AUM) — critical for NBFCs

-

Debt-to-equity ratio

-

Interest coverage ratio

-

Cash flow consistency

Large issuers such as Bajaj Finance, Shriram Finance, and Tata Capital regularly access bond markets and publish financial disclosures.

4. Remaining Tenure

Maturity

The shorter the time to maturity, the lower the probability of credit risk (generally).

-

6 months – 2 years → Lower uncertainty

-

3–5 years → Balanced

-

7–10+ years → Higher duration risk

If you are investing in slightly lower-rated bonds in India, shorter maturities are often preferred.

Maturity

Match bond maturity with your goal timeline:

-

Wedding in 2 years? → 2–3 year bond

-

Retirement income? → Laddered maturities

-

Parking surplus? → Short-term bonds

5. Listed & Regulated

Always ensure bonds are:

✔ Listed on NSE/BSE

✔ SEBI regulated

✔ Available via compliant platforms

OBPPs are SEBI-registered digital platforms that allow transparent bond investing.

Investing Through OBPPs in India

SEBI introduced the OBPP framework to make bond investing more transparent and accessible to retail investors.

Aspero

Aspero is a SEBI-registered Online Bond Platform Provider offering:

-

35+ bonds across AAA to BBB ratings

-

Short-term to long-term maturities

-

Monthly and quarterly payout options

-

Minimum investment starting from just ₹400

-

Senior secured, PSU, NBFC and corporate bonds

This allows retail investors to diversify across issuers, ratings, and tenures — something that earlier required ₹1 lakh+ ticket sizes.

Other OBPPs

Other SEBI-registered platforms include:

However, bond availability, ticket size, and diversity may vary across platforms.

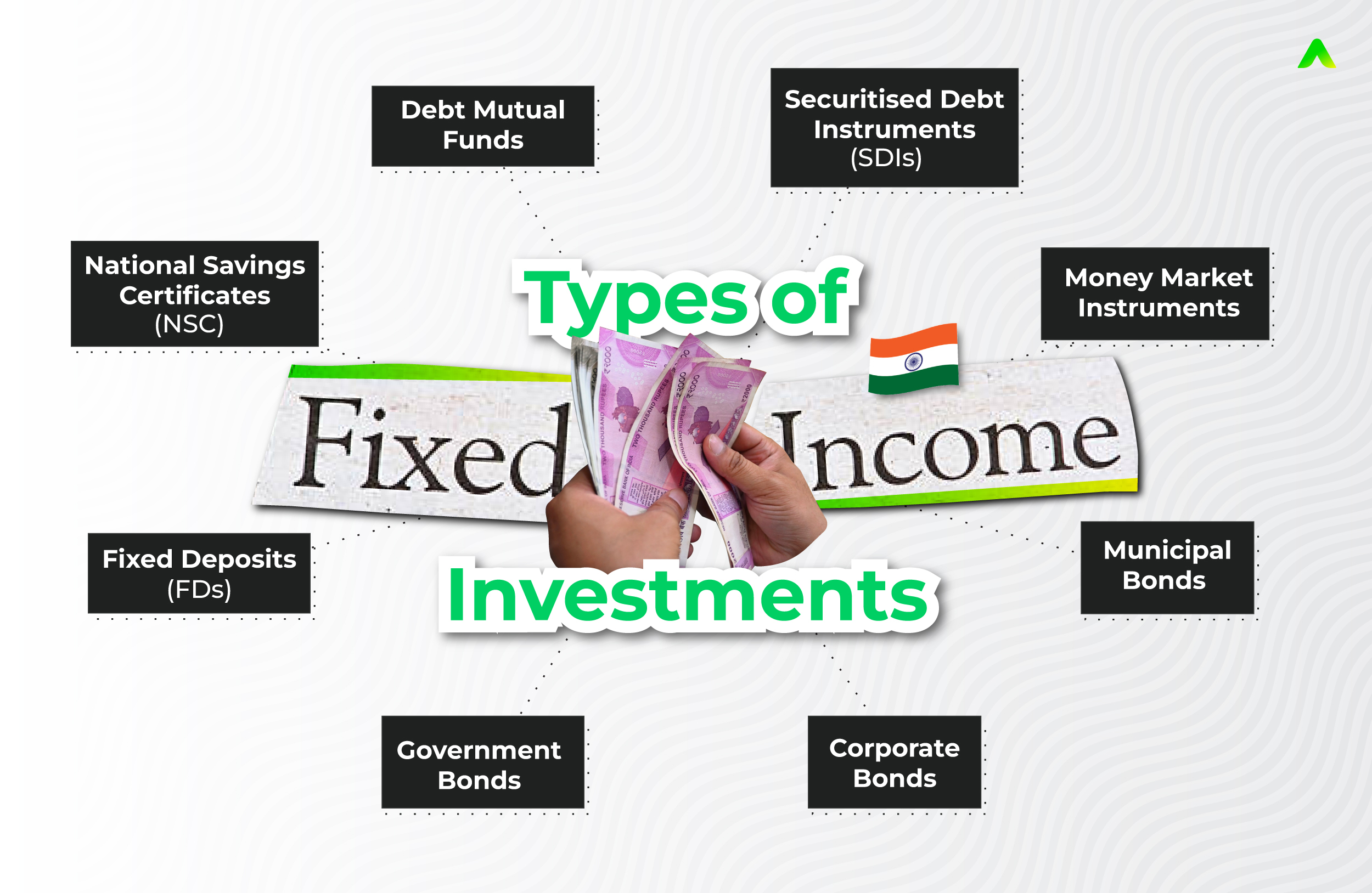

Government Bonds in India

Government bonds in India are issued by the Government of India via RBI.

You can invest through:

-

RBI Retail Direct

-

OBPP platforms like Aspero (where listed)

Types include:

-

G-Secs (10-year, 20-year, etc.)

-

Treasury Bills (91/182/364 days)

-

State Development Loans (SDLs)

These are considered among the safest fixed-income instruments.

Tax Basics for Bond Investors

Listed Bonds in India:

-

Interest income → Taxed as per income slab

-

Capital gains if sold before maturity:

-

Long-Term: 10% (without indexation)

-

Short-Term: Slab rate

-

Unlisted Bonds in India:

-

Interest: Taxed at slab rate

-

Long-term gains after 36 months: 20% with indexation

Tax planning can improve effective returns.

How Bonds in India Fit Different Investor Profiles

1. For Short-Term Income

Corporate bonds in India (1–3 years) offering monthly/quarterly payouts at ~9–13% yields.

Suitable for:

-

Wedding expenses

-

Vacations

-

Parking equity profits

2. For Retired Parents

Instead of relying only on FDs (6–7%), AA/A-rated bonds offering ~9%+ payouts can provide:

✔ Better income

✔ Predictable cash flow

✔ Lower volatility vs equity

3. For Young Professionals

Allocate 10–20% of portfolio to bonds.

Benefits:

-

Emergency fund parking

-

EMI coverage

-

Reducing equity volatility

-

Generating passive income

Market Experts on Bond Selection

✔ Always verify issuer fundamentals — even for high-rated bonds

✔ Prefer shorter maturities when taking higher credit risk

✔ Diversify across issuers and ratings

✔ Avoid over-allocation to high-yield or unrated bonds

✔ Use regulated OBPP platforms like Aspero for transparency

Final Thoughts

India’s bond market is growing rapidly, and retail participation is increasing due to digitization and SEBI regulation.

With platforms like Aspero offering:

-

35+ bonds

-

AAA to BBB spectrum

-

Monthly & quarterly payouts

-

Investments starting from ₹1,000

Bond investing is now accessible, diversified, and structured for Indian retail investors.

If chosen thoughtfully, bonds in India can:

-

Provide regular income

-

Reduce portfolio volatility

-

Support short-term and long-term financial goals

-

Complement equity investments